Management focused on cost of capital Capital policies for an optimal balance of growth investment, shareholder return, and strong financial foundation

Our objective is to use the imaging technology that we have cultivated since our foundation to help people achieve their purpose and well-being, and to realize a sustainable society. To fulfill that objective, my greatest mission as CFO is to execute the most effective long-term capital policy (financial strategy) for generating sustained growth in our corporate value by providing a combination of new value for human society (social value) and business growth (economic value). In our capital policy, I am particularly focused on boosting our ability to generate cash flow and improving our capital efficiency, as represented by ROE and ROIC. My aim is to establish the optimal capital and debt composition by improving our capital efficiency and controlling our capital costs while preserving the right balance of growth investment, shareholder return, and a strong financial foundation.

Improving capital efficiency guided by KM-ROIC and return from invested capital

In fiscal 2019, ROE and ROIC declined significantly due to Workplace Hub and the bio-healthcare business, and other new businesses taking longer to gain traction than we initially anticipated along with the inevitable impacts on both revenue and profit owing to the worldwide spread of the COVID-19 pandemic, which constrained our sales activities, particularly in Europe and the United States where we have competitive presence.

The present status of the COVID-19 pandemic suggests fiscal 2020 could be even more challenging for our business. Our plan is to intently focus on raising ROE and ROIC back above our capital costs by building our business momentum and maximizing business profit in relation to business assets (return from invested capital).

Specifically, beginning in fiscal 2020, we will use KMROIC*1 and return from invested capital*2 as our primary management indicators for raising capital efficiency. We are using KM-ROIC as a benchmark as we transform our business portfolio, and return from invested capital will be integrated to the performance assessments used to determine manager bonus payments and to gauge the management of our group subsidiaries companies.

We are therefore shifting our performance management from centering on earnings to focusing on the efficiency of our capital investments. We will engage the whole company in activities to improve capital efficiency by using e-learning to provide examples of ways to improve capital efficiency and to raise awareness about capital costs among all employees and managers. We will also deepen and strengthen our operations and broaden their range of application in the medium term, while constructing a flexible financial base that is resilient to severe market conditions and will enable us to maximize our corporate value.

*1KM-ROIC is business profit divided by invested capital. It indicates the rate that business investment is generating business profit.

*2Return from invested capital is business profit minus the cost of invested capital. It indicates how much value has been created above the cost of invested capital.

Capital expenditure and investment and loans to generate cash flow

As we transform the Group’s business portfolio, we are focusing on generating operating cash flow by improving the profitability of the core business and the efficiency of our working capital. At the same time, we plan to use effectively use capital expenditure and investment and loans to maximize free cash flow.

In fiscal 2019, our capital expenditure totaled ¥50.8 billion. Principal investments were for machinery and equipment, molding dies, and other tools and appliances in the Office and Professional Print businesses, machinery and equipment in the Industrial Business, and buildings and R&D equipment for company-wide use. Investment and lending totaling ¥7.9 billion, which was mainly used to acquire a Spanish company developing an automotive visual inspection business in the Industrial Business. We used our own resources to fund the majority of our investments during the year.

Our investment plans for fiscal 2020 center on the Digital Workplace Business, Professional Print Business, and Industry Business. We plan to execute judiciously selected strategic investment to expand our production capacity, prepare to manufacture new products, retool our domestic production sites, strengthen our development capabilities globally, and execute judiciously selected strategic investment to optimize the efficiency of our operating sites in the Kansai area.

Enhancing shareholder return

Our basic policy on shareholder return is to actively return profit to shareholders while taking into account the overall status of the Company, including our consolidated performance and our ability to conduct the strategic investment in growth fields. We also seek to enhance shareholder return through higher dividends and by flexibly repurchasing company shares.

Despite recording a net loss in fiscal 2019, the Company distributed interim dividends per share of ¥15 at September 30, 2020, and ¥10 at the year end for a total annual dividend payment of ¥25 per share. We forecast posting a net loss again in fiscal 2020 owing to the impact of the COVID-19 pandemic. However, we believe measures to improve profits in the Office Business and new businesses and steps to maintain the reduced level of fixed costs give us a strong probability of regaining the pre-pandemic profit levels in fiscal 2021 and 2022. Based on this outlook, we plan to maintain the fiscal 2019 dividend payment rate and forecast providing

a total annual dividend payment of ¥25 per share in fiscal 2020.

Solidifying our financial foundation

We are creating a solid financial foundation to support our aggressive investment in growth by strengthening our financial governance, minimizing financial risk, improving capital efficiency, and enhancing shareholders’ equity.

The main source of funds needed to ensure smooth business activities are the cash flow generated by our operating activities, and we supplement this by securing ready liquidity through short- and long-term loans from financial institutions and by issuing corporate bonds while maintaining our financial soundness and stability. Financial risk associated with long-term financing is reduced by dispersing the periods for redemption and repayment. In addition, the procurement of funds is centralized and made more efficient by having the Company be the primary arranger for the Group and supplying the necessary funds to affiliated companies through a cash management system.

The Company maintained a cash and cash equivalents balance of approximately ¥90 billion at the end of fiscal 2019 and in April 2020 secured an additional ¥85 billion in loans from financial institutions as a precaution due to the uncertainty associated with the COVID-19 pandemic. We additionally have unused commitment lines from multiple financial institutions totaling ¥300 billion (as of end-May 2020). We believe these preparations will ensure sufficient liquidity to deal with any impacts on our businesses from the coronavirus.

The Rating Investment Information Center (R&I) and Japan Credit Rating Agency (JCR) have given ratings of A to the Company’s corporate bonds and preliminary ratings of A to future bond issues by the Company.

Business Portfolio Management Strengthening our business portfolio management guided by KM-ROIC

The proliferation of tablet computers, smartphones, and other electronic equipment coupled with workstyle changes has accelerated the shift in offices from paper to digital data in recent years. We are responding to this fundamental change in the office environment by overhauling our business content, particularly in our core Office Business, with an outlook for the medium and long term. During the two medium-term management plans over the past six years, we have transformed our business composition through aggressive investment in Workplace Hub, industrial printing, bio-healthcare, visual inspection, and the new field of status monitoring solutions.

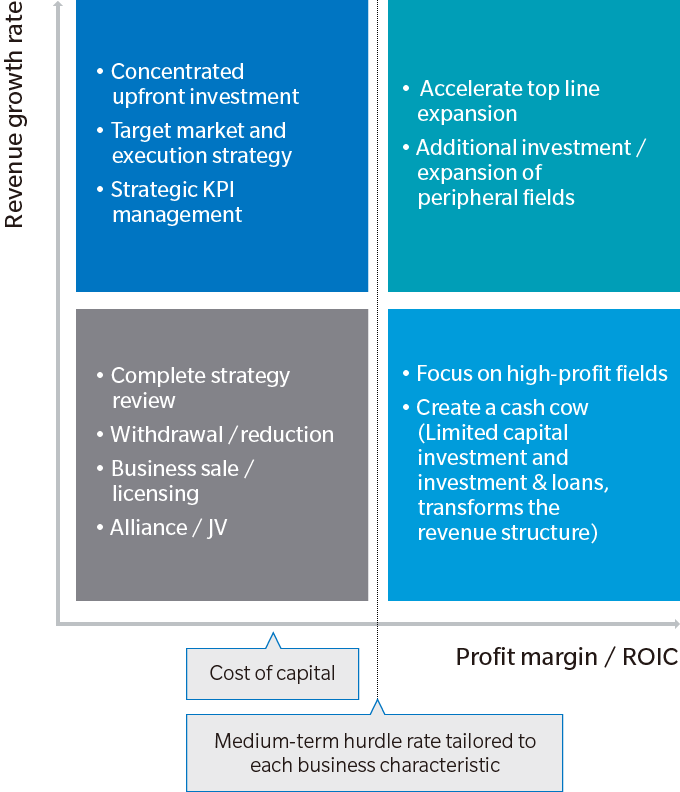

The new DX2022 medium-term business strategy starting in fiscal 2020 calls for continuing with the selective upfront investment in the domains essential to our future growth, specifically the Digital Workplace Business and the precision medicine and measurement instruments business units, while also improving capital efficiency and maximizing corporate value by putting greater emphasis on maximizing the return from past investments and optimizing the business portfolio to improve capital efficiency.

Optimizing our business portfolio is being executed by assessing each of our businesses in terms of business attractiveness, sustainable competitiveness, and adaptability of the corporate strategy. One of the main indicators we are using to assess business attractiveness is the KM-ROIC mentioned above. Taking into account the actual invested capital efficiency at each business unit level along with the average in the industry, we are setting medium-term hurdle rates for the KM-ROIC expected of each business and will gear our business strategies and operations toward surpassing those minimum targets. The ability to meet hurdle rates for investment return will also be criteria when starting new businesses and investments. We will also periodically review the KM-ROIC of investments with the aim of eliciting maximum return.

We will also consider withdrawing from or downsizing businesses following exit rules with specific baselines for business profitability, investment capital efficiency, and other items. If monitoring reveals a business has fallen below these baselines, the business will be deemed a withdrawal candidate, and we will commence a close examination of the benefits of withdrawing from the business. Cash acquired from selling a business will be added to our investment strategy for growth and to optimize the business portfolio, improve capital efficiency, and increase cash flow for the medium and long term.

We will continue aggressively overhauling our business portfolio guided by our objectives to improve the efficiency of our invested capital and to bring about our digital transformation.

Evaluating “business attractiveness” with an awareness of capital costs

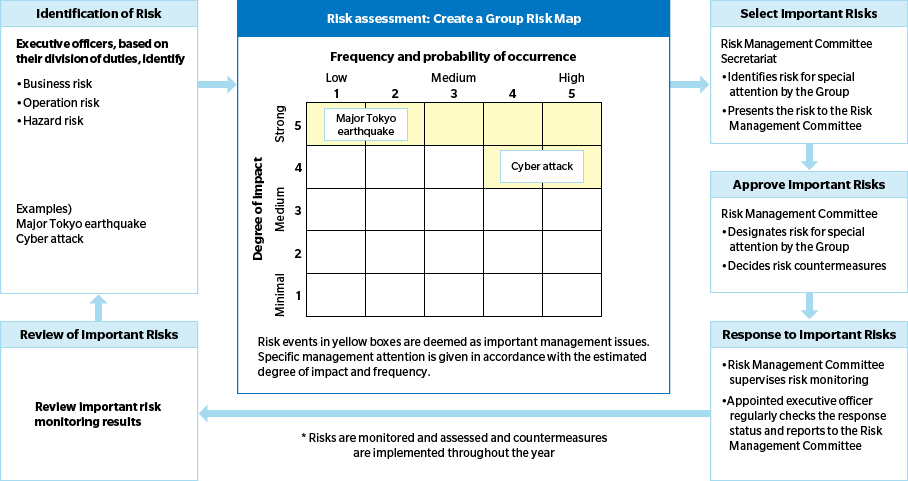

Risk Management Major risks identified by frequency and potential degree of impact

The Company’s Risk Management Committee is charged with the overall and systematic management of the potential risks to the Group’s businesses, including formulating and strengthening the risk management structures of each Group company. As the committee chair, I appoint corporate executives with positions of executive officer or higher to serve as committee members whose duties include executing the risk management associated with their corporate duties. At biannual meetings, the committee updates the Group Risk Map created based on our risk classification system to represent the potential impact and frequency for each department and discusses countermeasures. The chairman convenes a meeting of the committee as deemed necessary in the event an unforeseen risk circumstance arises. The committee reviews the status of countermeasures for risks assessed as high importance on a monthly and quarterly basis, and the committee chairman appoints an executive officer to supervise the Group response for risks considered of critical importance.

We consider risk to be any situation that presents “uncertainty” about a potential impact on the earnings of our organization. In that sense, risk management encompasses not just the negative side of risk but also the positive side for our sources of earnings. It is therefore essential for mitigating potential negative impact as well as for pursuing the maximum return from opportunities.

Process of Identifying Important Risk for the Group

The COVID-19 pandemic is a case in point. Although it is substantially affecting our sales activities, early recognition of the potential risk led our CEO to activate the company’s Temporary Crisis Management System in January 2020. This put priority on the health and safety of our employees and their families, customers, business partners, and all stakeholders and that eventually enabled us to resume factory operations at a relatively early date.

We have also looked ahead to when economic activity returns and envision medical professionals needing more support than before and an overall change in people’s values and work styles.

The business growth we have seen as we helped address such a major social issue as the coronavirus shows that such activities are positives for the Company. Our business has grown from assisting in AI diagnosis of chest X-rays and remote medical diagnosis, commercializing PCR testing in the United States, using Workplace Hub to facilitate multi-site collaboration and new work styles, providing expertise gained from our in-house teleworking system, and providing AI-integrated thermal cameras for body surface temperature readings.

The changes in the earth’s environment is another risk as climate change and abnormal weather activity around the world threaten our business continuity and could impact our future earnings. Recognizing these risks, we are doing our part to mitigate global warming. The Group is committed to becoming “Carbon Minus” by lowering its CO2 emissions below the levels of our customers, suppliers, and local communities. We have set ambitious targets to have reduced the CO2 emissions from our product lifecycles by 60% in 2030 and 80% in 2050 compared to fiscal 2005. Konica Minolta discloses information about its business risk and opportunity related to climate change in accordance with the framework of the Task Force on Climate-related Financial Disclosures.

Properly managing the various risks from a medium- and long-term perspective is a key part of our efforts to establish sustaining growth in corporate value.

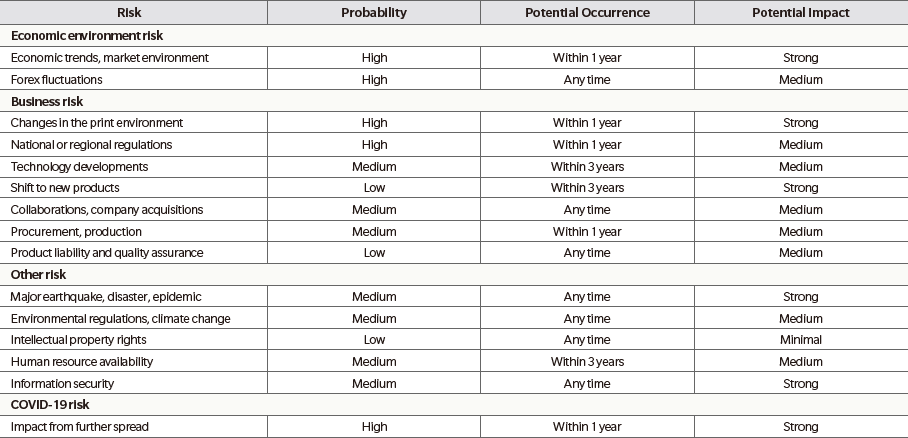

Business Risk