Prioritizing two portfolio transformations

Our core Office Printing Business has seen a continued drop off in printing demand in recent years, and in fiscal 2020 this trend accelerated due to the COVID-19 pandemic. To address this change in business environment, we are now working to transform two different portfolios simultaneously. The first shift involves evolving the Office Printing Business, which had focused on MFPs, into the Digital Workplace Business, and the second is establishing the measurement, inspection and diagnostics domains as new pillars of business. At present, the top priority of management is quickly achieving these two portfolio transformations, with completion slated by fiscal 2025.

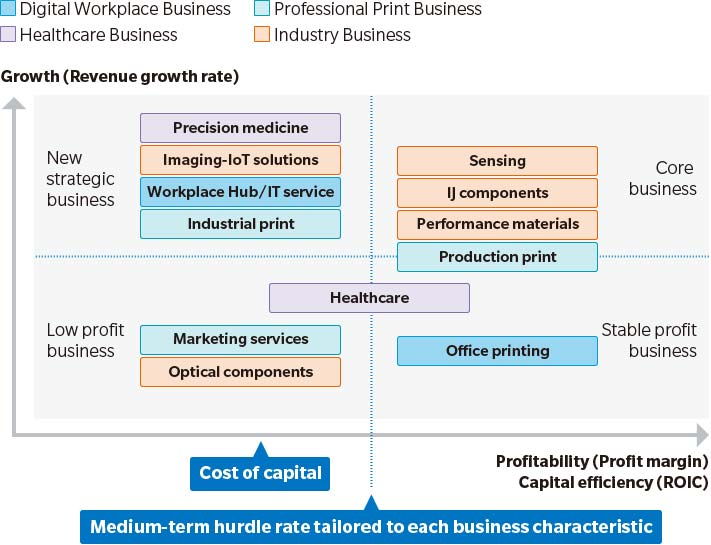

In our business portfolio management, we have rigorously evaluated the importance and role of each business according to the three areas of growth, profitability/capital efficiency and compatibility with strategy. Based on the results, we are mapping each under the quadrants of new strategic business, core business, stable profit business, and low profit business. We will take concrete action in allocating investments and resources to businesses vital to this business portfolio transformation. For low profit businesses, we plan to place every option on the table, including selling off the business or pursuing a capital tie-up with a third party, for improving profitability and selecting targeted businesses. In this manner, we will take action promptly, efficiently and in a dynamic nature.

Business portfolio management focused on capital efficiency

In terms of improving our business portfolio management, we are working to maximize corporate value and increase company-wide capital efficiency using the KPI of business-unit specific KMROIC*1 and company-wide capital cost. Specifically, we have set KM-ROIC (hurdle rate) for each business that needs to be achieved during DX2022, and now each business is implementing business strategy aimed at achieving this KPI. When reviewing the launch of new businesses or M&A, the period required for each deal’s KM-ROIC to exceed the company-wide hurdle rate is used as one of the important criteria for judging whether to move forward with an investment. Furthermore, we aim to generate a return beyond the initial target while regularly reviewing the situation even after the investment is completed.

Meanwhile, we have established exit rules, such as falling below the business-unit specific hurdle rate and capital cost, for determining when to exit or scale down a business. Businesses that breach these rules will undergo a detailed review process for restructuring or exit.

We consider business-unit specific KM-ROIC and return on invested capital*2 to be foundations for the enhancement of company-wide capital efficiency. Through maximizing both, we will further enhance capital efficiency and corporate value.

*1 KM-ROIC is business profit divided by invested capital. It indicates the rate that business investment is generating business profit.

*2 Return on invested capital is business profit minus the cost of invested capital. It indicates how much value has been created above the cost of invested capital.

Business Portfolio Management

Setting financial targets and KPI for financial soundness

Under DX2022, we have established targets for each fiscal year covering not only profits, but also ROIC and financial soundness. However, our top priority is completing the two portfolio transformations mentioned above by fiscal 2025. Therefore, we intend to make strategic investments ahead of time as needed going forward. During this process, achieving the targets for ROIC and financial soundness could become a slightly lower priority.

Of course, we will maintain the target of restoring ROIC to a level higher than 6.5% in excess of capital cost by the end of fiscal 2025 along with the basic policy of aiming for ROIC of between 9% and 10% over the long term. There is also no change in our approach of further solidifying our financial foundation by strengthening financial governance, minimizing financial risks, improving cash efficiency, and boosting shareholders’ equity and using this to support aggressive investments in growth during the timeline until fiscal 2025.

Capital policy for growth

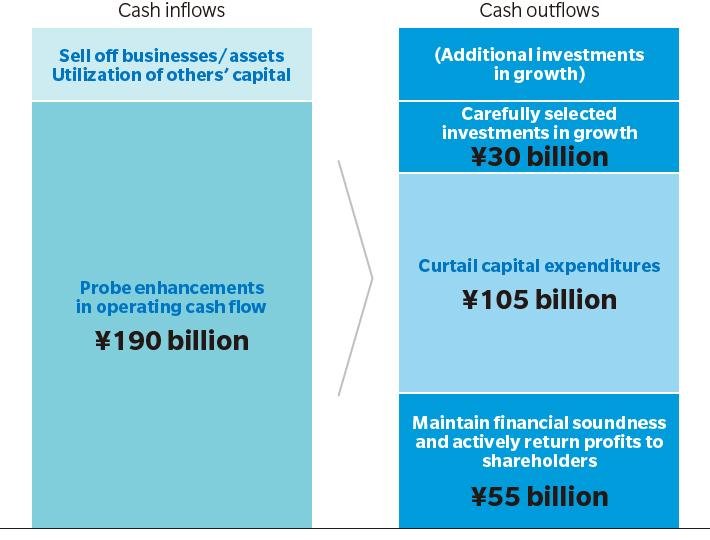

Operating cash flow has seen a strong recovery since the second quarter of fiscal 2020. Looking ahead, we will work toward generating ¥100 billion in operating cash flow per year by working toward comprehensive improvements in the successful undertaking of structural reforms and efficiency measures, boosting the profitability of new businesses, and the cash conversion cycle through further reducing inventories and trade receivables. Moreover, we plan to maximize cash inflows by either carving out non-core businesses and assets or seeking out capital tie-ups to accelerate upscaling.

We will earmark the cash generated for strategic investments in future growth in the amount of around ¥30 billion over the two fiscal years of 2021 and 2022. We intend to concentrate investment on business domains slated to become the next pillars of our growth, and we will also explore the possibility of executing investments planned for fiscal 2023 and later ahead of time in order to complete our business portfolio restructuring by fiscal 2025.

In terms of capital expenditures, we will take a dynamic approach, where we rein in capital expenditures in the Office Printing Business, but at the same time increase spending directly tied to DX and business growth. We will also strive to reduce debt after considering the optimal balance between growth investments and financial soundness.

Approach to cash allocation for fiscal 2021/fiscal 2022

Shareholder returns

Our basic policy regarding shareholder return is to proactively distribute earnings to shareholders after comprehensive consideration of factors including consolidated business results and strategic investment in growth areas. For fiscal 2020, we paid a dividend of ¥25 per share, consisting of a ¥10 interim dividend and ¥15 year-end dividend.

In fiscal 2019 and fiscal 2020, we prioritized liquidity on hand because of the unprecedented nature of the COVID-19 pandemic, which forced us to reduce our dividend below the ¥30 per share level that we had maintained for some time. However, we have seen a steady recovery in our profits and ability to generate cash since the second quarter of fiscal 2020. As a result, we are making solid progress toward achieving our management plan targets for fiscal 2021 and beyond.

We expect to be able to restore the annual dividend to ¥30 per share in fiscal 2021. Looking forward, we are committed to making steady progress toward further enhancing corporate value.